{kind=link}

The government’ is to protect and revitalise the private sector by shifting from a culture of liquidation to one of rescue and rehabilitation.

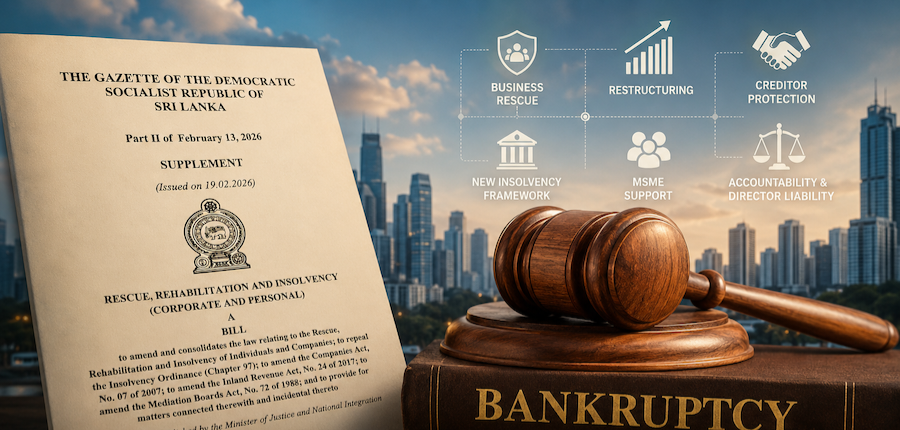

In this context the Rescue, Rehabilitation and Insolvency (Corporate and Personal) Bill will be presented in Parliament soon, representing a major modernisation of Sri Lanka’s outdated 1853 Insolvency Ordinance.

It is introducing modern legal frameworks to provide “breathing space” for distressed businesses rather than immediate bankruptcy, justice ministry sources revealed.

This Bill introduces an administration regime to allow qualified administrators to manage struggling companies while temporarily pausing enforcement actions by creditors, creating room for restructuring.

The formation of a dedicated body will help to professionalise insolvency, thus ensuring that the practitioners adhere to the principles of ethics and transparency in their dealings in the business reorganisation process.

In view of the fact that Micro, Small, and Medium Enterprises (MSMEs) account for more than 52 percent of the GDP,

The proposed bill incorporates an easy mechanism of restructuring that is tailor-made for small companies that cannot afford complicated corporate processes.

It is considered crucial for improving the investment climate and helping businesses manage distress after economic turbulence.

The government’s aim is to reduce the “cost of doing business” through digital transformation.

A digital platform is being developed to streamline the approval process for investors, aiming to replace bureaucratic delays with a transparent, “one-stop-shop” technology.

The National Export Development Plan 2025–2029 focuses on integrating local private companies into global value chains, specifically in high-potential sectors like ICT, gems, and electronics.